Even as Microsoft's (MSFT) stock has been flat or down this month since the GitHub acquisition, I believe in the long-term GitHub has significant chances in boosting a variety of Microsoft software and Internet services segments, even outside of cloud computing, to help it successfully compete and still grow.

Furthermore, Microsoft's valuation metrics, stock characteristics, and largely steady business outside of cloud all makes its downside risk low in my opinion aside from a market-wide downturn.

With Microsoft Azure and its cloud segment as a whole continuing to show strong expansion in a still-rapidly growing sector, with the low potential drop-risk, make it have an exciting upside that could manifest itself in significant gains.

(Source: The Verge)

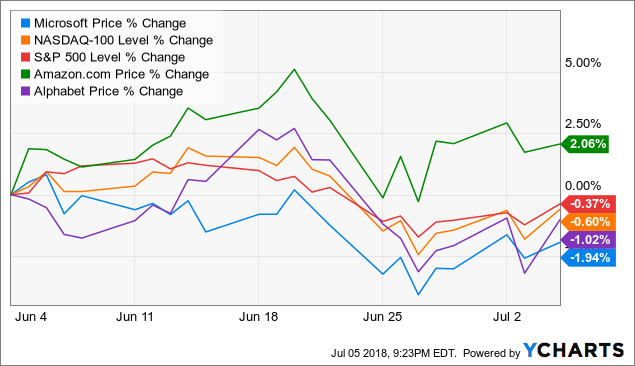

GitHub, Cloud Computing, And Staying Competitive In A Constantly Rapidly Innovative SectorLast month I discussed with members of Tech Investment Insights why I believe Microsoft's acquisition of GitHub could be disruptive to not only its cloud segment but all its software business lines. While Microsoft stock since then has been relatively stagnant, even declining slightly beyond the broader market indexes' declines.

MSFT data by YCharts

MSFT data by YCharts

I think however GitHub will begin to contribute slightly to Microsoft's bottom line itself as a segment in upcoming earnings quarters, but more particularly its innovative potential augmentation of the development of Microsoft's other software segments.

GitHub, as a hosting, development, and collaboration platform for code, is immensely valuable to Microsoft in its potential to push efficiencies and innovation. While the $7.5 billion acquisition cost seems high, that it will be in stock both lessens the otherwise potential debt burden on Microsoft and explains partially why the stock has been slightly depressed the past month.

Nonetheless, at a current market cap of over $766 billion the $7.5 billion in stock acquisition cost won't be much of a long-term transformation of shareholder equity.

Given that apparently the GitHub deal had already mostly closed by its leak in early June, with the final terms expected to fully close by the end of the year, we could see it begin to make an impact even sooner than expected.

Yet the primary benefit for GitHub remains in the long-run as a way to keep Microsoft's software capabilities competitive, particularly against its innovative challengers Amazon (AMZN) and Google (GOOGL) in cloud.

(Source: CNBC)

As I've previously discussed, cloud computing has been immensely profitable for Microsoft as a high-margin product despite its current size. Just like with Amazon, cloud has helped even these massive companies see significant earnings growth even at their current enormous market caps.

The cloud computing sector is expected to continue to expand at rapid levels and Microsoft has been slowly gaining market share in it, even though with the vast amounts of sector growth happening market share is not as essential as for a mature industry.

GitHub's boost will slowly manifest itself over time in unpredictable ways, as innovation and research development often is a constant hit-or-miss chance cube. It likely still will have enough brain trust power to create major benefits to Microsoft's cloud computing competitiveness and even potentially its other various Internet services and software products, possibly including its unclear but determined forays into the cryptocurrency and Blockchain sector.

MSFT data by YCharts

MSFT data by YCharts

Valuation-wise, Microsoft currently stands at a TTM price-to-earnings ratio of 27.50 based on GAAP EPS of $3.60. There is only 0.73% in short interest and over 72.19% of the stock is held by institutions, which in my opinion demonstrates a firm and steady floor for the company's stock as well.

Even if significant accelerated growth does not materialize, the P/E ratio is only very slightly a growth-ratio and the stocks other characteristics do not give the appearance of major downside risk, barring market-wide downturns.

One market-wide factor that is currently creating wider turbulence and particularly among tech companies are tariffs. Though the global tariffs conflict could be disruptive to Microsoft activities in building its data-centers and the few hardware products it does shift, it seems at the moment many of its cloud computing, software, LinkedIn, and other product lines may not be affected significantly.

ConclusionOverall, I believe Microsoft was already on a slight growth trajectory before GitHub's acquisition, due to the effect of its cloud computing segment and stability of its other business lines.

GitHub's acquisition upgrades that to a more moderate growth expectation, as GitHub could potentially create widespread and long-lasting innovative advancements that helps Microsoft compete in cloud and other software and Internet services business lines.

Furthermore, I see little downside risk in the company unless there is a wider market downturn in which case the company can only resist the tide so much. In the meantime it appears the company has strong ins

No comments:

Post a Comment